{kind=link}

Master Trust Pension Compliance

Master Trust Pension Compliance

4

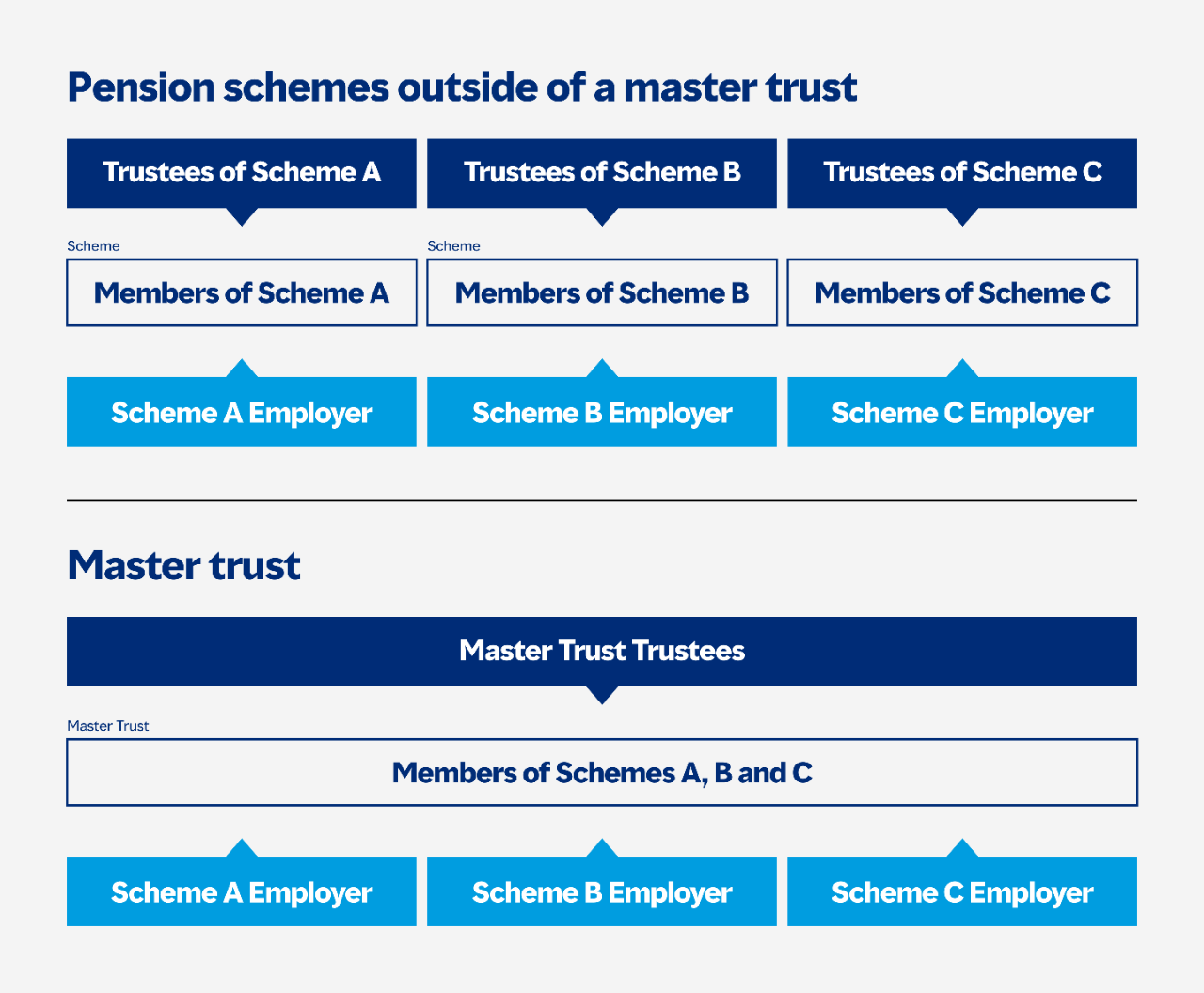

Master trust pension schemes are occupational pension arrangements where multiple, unrelated employers participate under a single trust structure. They are widely used for defined contribution (DC) pensions, especially for auto-enrolment regimes. Because they pool assets and governance, regulators impose strict compliance frameworks to protect members.

1. What is a Master Trust?

A master trust is a multi-employer pension scheme:

- Established under a single trust deed

- Managed by trustees who act in members’ best interests

- Operated by a scheme funder/provider

- Used by numerous employers who are not related

Key Participants:

- Trustees

- Scheme funder

- Participating employers

- Members (employees)

2. Regulatory Framework (Global Overview)

United Kingdom

- Governed by the Pension Schemes Act 2017

- Supervised by The Pensions Regulator

- Requires authorization and ongoing supervision

European Union

- IORP II Directive (Institutions for Occupational Retirement Provision)

India

- Regulated under Pension Fund Regulatory and Development Authority (PFRDA)

- National Pension System (NPS) structures resemble pooled pension frameworks

3. Core Compliance Requirements

3.1 Authorization & Licensing

Master trusts must demonstrate:

- Financial sustainability

- Fit and proper persons managing the scheme

- Adequate systems and processes

Failure leads to regulatory intervention or winding-up.

3.2 Trustee Duties & Governance

Trustees must:

- Act in fiduciary capacity

- Avoid conflicts of interest

- Ensure proper investment decisions

- Maintain transparency with members

3.3 Financial Sustainability

- Scheme funder must have sufficient capital

- Contingency plans for financial failure

- Protection of member funds

3.4 Administration & Record-Keeping

- Accurate member records

- Timely contributions processing

- Data protection compliance

3.5 Investment Governance

- Diversified investment strategy

- Risk management systems

- ESG considerations (in some jurisdictions)

3.6 Continuity Strategy

- Plans for:

- Scheme failure

- Transfer of members

- Wind-up procedures

3.7 Member Communication

- Clear disclosure of:

- Fees

- Investment risks

- Benefits

4. Key Compliance Risks

- Mismanagement of pooled assets

- Conflicts between scheme funder and trustees

- Inadequate capitalization

- Data breaches and record errors

- Failure to meet regulatory authorization standards

5. Enforcement Mechanisms

Regulators may:

- Issue fines or penalties

- Remove trustees

- Withdraw authorization

- Force scheme wind-up

- Initiate criminal proceedings (in severe cases)

6. Leading Case Laws (At Least 6)

6.1 Imperial Group Pension Trust Ltd v. Imperial Tobacco Ltd (1991, UK)

- Established limits on employer interference

- Reinforced trustee independence in pension schemes

6.2 Edge v. Pensions Ombudsman (1999, UK)

- Clarified trustees’ discretionary powers

- Emphasized acting in members’ best interests

6.3 Cowan v. Scargill (1985, UK)

- Landmark ruling on investment duties

- Trustees must prioritize financial interests of beneficiaries over personal views

6.4 Hughes v. Royal London Mutual Insurance Society Ltd (2016, UK)

- Addressed fairness and communication in pension administration

- Highlighted importance of transparency

6.5 Re National Grid Co plc (2001, UK)

- Concerned surplus distribution in pension schemes

- Demonstrated fiduciary obligations in fund management

6.6 IBM United Kingdom Holdings Ltd v. Dalgleish (2017, UK)

- Examined employer obligations and member expectations

- Introduced the concept of “reasonable expectations” in pension changes

6.7 Arcadia Group Pension Trust Ltd v. Smith (2014, UK)

- Focused on trustee decision-making and conflicts of interest

- Reinforced governance standards

7. Best Practices for Corporate Compliance

7.1 Governance Framework

- Independent trustee boards

- Clear separation from scheme funder

7.2 Risk Management

- Regular compliance audits

- Stress testing financial sustainability

7.3 Technology & Data

- Secure digital record systems

- Automated contribution tracking

7.4 Transparency

- Regular member reporting

- Clear disclosure of fees and risks

7.5 Regulatory Engagement

- Proactive communication with regulators

- Early reporting of issues

8. Comparative Perspective

| Aspect | Master Trust | Single Employer Scheme |

|---|---|---|

| Employers | Multiple | One |

| Governance | Centralized trustees | Employer-linked |

| Risk | Shared | Employer-specific |

| Regulation | Stricter | Moderate |

9. Conclusion

Master trust pension compliance is a highly regulated area due to the scale and systemic importance of pooled retirement savings. Effective compliance ensures:

- Protection of member assets

- Stability of pension systems

- Trust in long-term retirement planning

For corporates, participation in master trusts requires careful due diligence, governance oversight, and regulatory alignment to avoid significant legal and financial exposure.

RELATED Blog

comments