{kind=link}

Put-Call Option Governance

Put–Call Option Governance (Corporate & Shareholder Context)

4

Put and call options are contractual rights commonly embedded in shareholders’ agreements, joint ventures, and private equity deals. They function as governance tools by allocating control over ownership transitions, exit rights, and risk management.

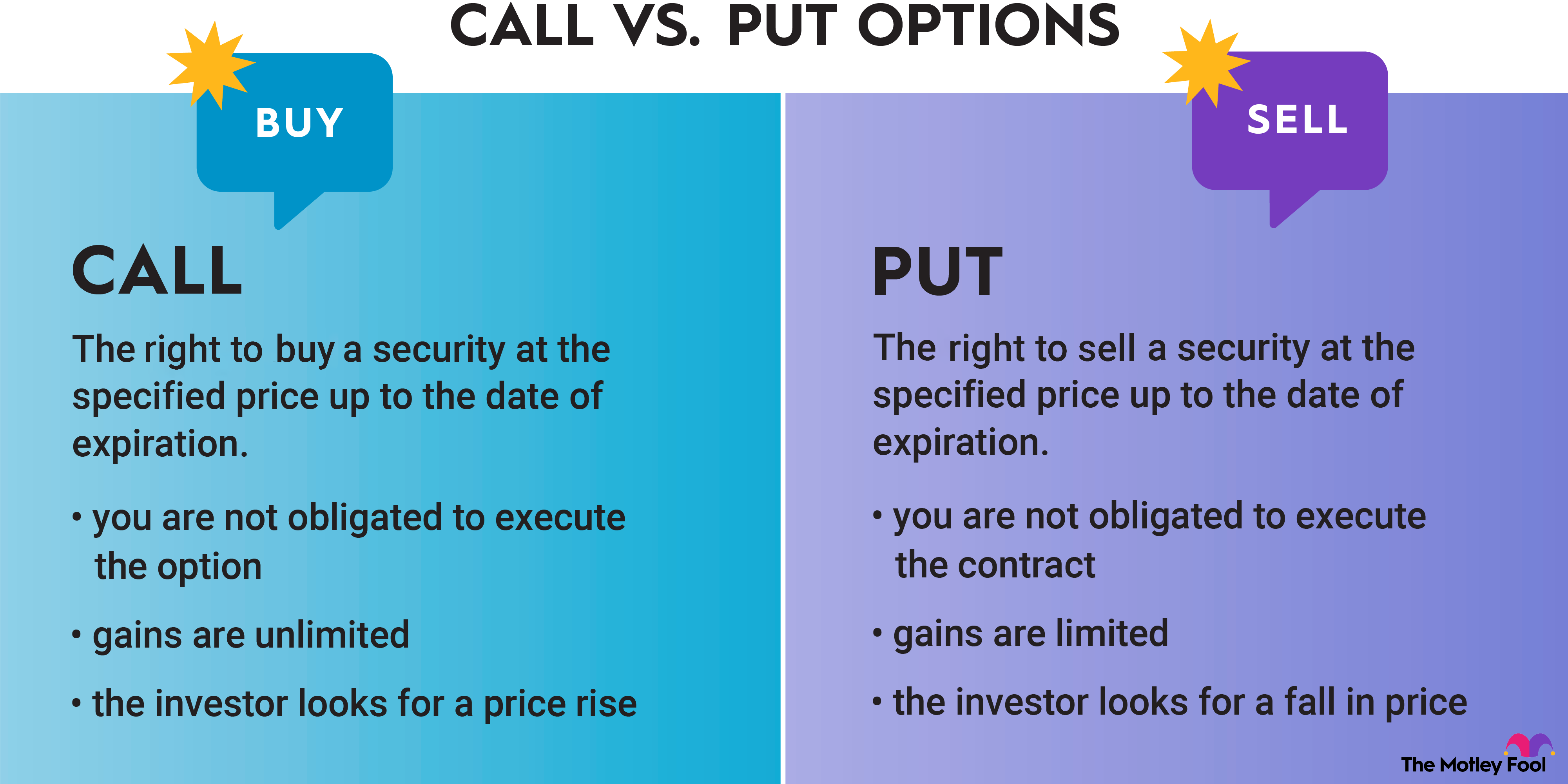

- Put Option → Right to sell shares at a predetermined price

- Call Option → Right to buy shares at a predetermined price

These mechanisms are not merely financial instruments; they are governance levers affecting control, minority protection, and dispute resolution.

1. Governance Functions of Put–Call Options

(a) Exit Mechanism

- Provides certainty of exit for investors (especially minority shareholders or private equity funds)

- Avoids deadlock or illiquidity in closely held companies

(b) Control Consolidation

- Call options enable majority shareholders to increase control

- Put options allow minority investors to force liquidity events

(c) Risk Allocation

- Pre-agreed pricing formulas distribute market risk

- Protects parties from opportunistic behavior

(d) Deadlock Resolution

- Often triggered upon:

- Management disputes

- Breach of agreement

- Change in control

2. Legal Nature and Enforceability

Put–call options are typically governed by:

- Contract law (binding agreements)

- Company law (share transfer restrictions)

- Securities regulations (especially for listed companies)

Key Issues:

- Whether options are speculative or enforceable contracts

- Compliance with transfer restrictions in articles of association

- Regulatory limits (e.g., SEBI in India, FCA in UK)

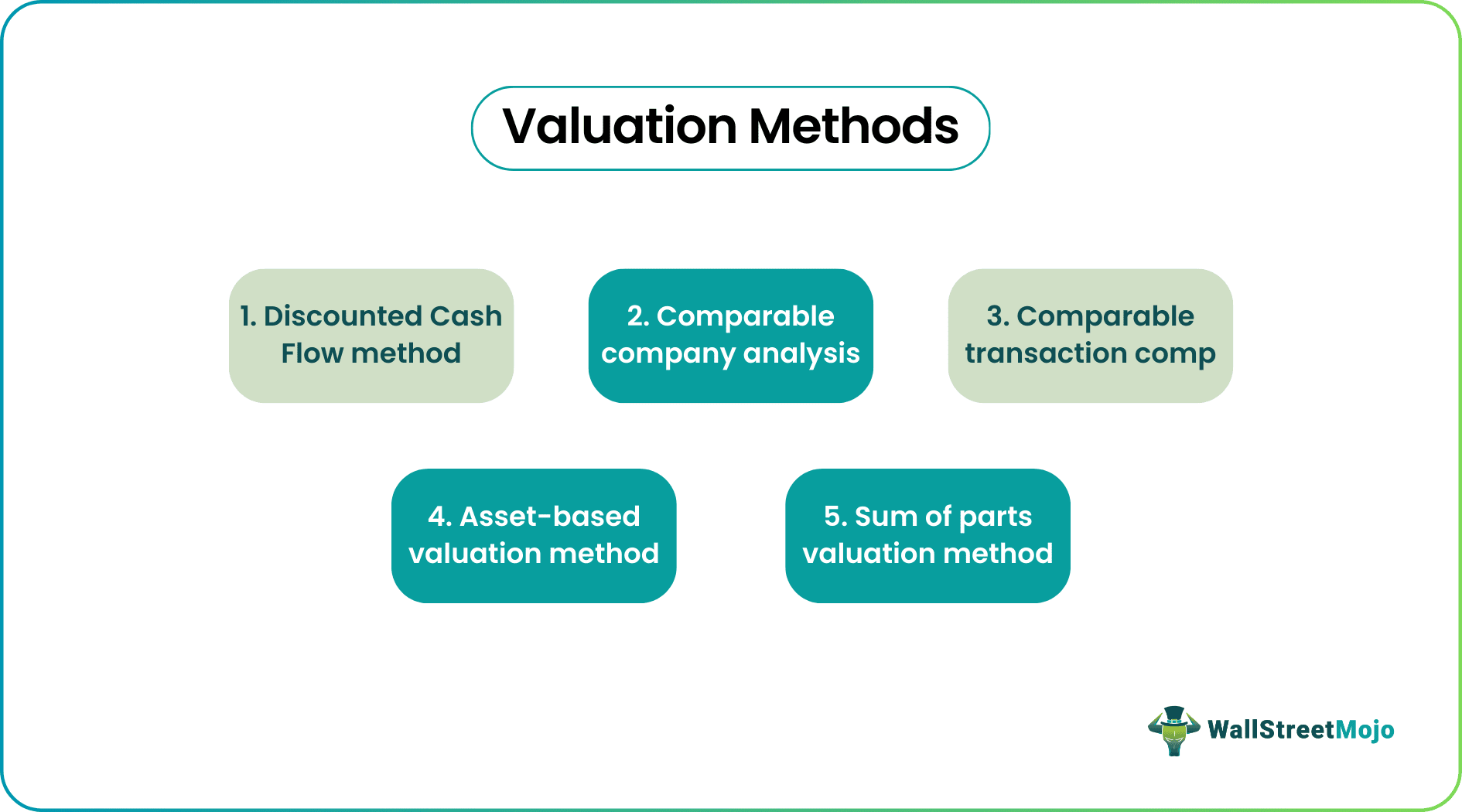

3. Pricing and Valuation Governance

4

Pricing mechanisms determine fairness and often lead to disputes.

Common Methods:

- Fair market value (FMV)

- Discounted cash flow (DCF)

- Pre-agreed formula (EBITDA multiples)

- Independent valuer determination

Governance Concern:

- Avoidance of unfair prejudice or minority squeeze-out

4. Interaction with Corporate Governance Principles

(a) Fiduciary Duties

Directors must ensure:

- Options are exercised in good faith

- No abuse of power to dilute minority shareholders

(b) Minority Protection

- Put options serve as exit protection

- Prevent “lock-in oppression”

(c) Proper Purpose Doctrine

- Exercise of options must not be for collateral or improper purposes

5. Key Case Laws (At Least 6)

1. Russell v Northern Bank Development Corp Ltd (1992, HL)

- Shareholder agreements restricting statutory powers may be unenforceable against the company but valid among shareholders.

- Important for structuring option clauses vis-à-vis company powers.

2. O’Neill v Phillips (1999, HL)

- Established principles of unfair prejudice.

- Relevant where refusal to honor exit (put option) harms minority shareholders.

3. Ebrahimi v Westbourne Galleries Ltd (1973, HL)

- Recognized equitable considerations in quasi-partnership companies.

- Put options often act as contractual substitutes for equitable remedies like winding up.

4. Re Coroin Ltd (2013, UKSC)

- Concerned enforcement of pre-emption and control rights.

- Demonstrates strict judicial scrutiny of contractual governance mechanisms affecting share transfers.

5. BP Exploration Co (Libya) Ltd v Hunt (No 2) (1979)

- Discussed valuation and restitution principles.

- Relevant in determining fair compensation in option-triggered exits.

6. Arbuthnott v Bonnyman (2015, UK)

- Addressed enforceability of share transfer provisions and valuation clauses.

- Courts uphold clear contractual mechanisms unless unfair or ambiguous.

7. VMR v Mustang Marine Ltd (2018, UK)

- Confirmed courts’ willingness to enforce commercial share option arrangements where clearly drafted.

8. Moorjani v Durban Estates Ltd (2015, UK)

- Highlighted disputes over valuation and minority exit rights, reinforcing importance of precise drafting.

6. Regulatory and Market Trends

(a) Increasing Use in Private Equity

- Standard feature in investment agreements

- Provides structured exit within 3–7 years

(b) Judicial Preference for Certainty

- Courts generally enforce clearly drafted options

- Ambiguity leads to litigation

(c) Scrutiny in Listed Companies

- Options may be regulated to prevent:

- Insider advantage

- Market manipulation

7. Governance Risks

4

(a) Minority Squeeze-Out

- Call options used unfairly to remove minority shareholders

(b) Undervaluation Disputes

- Manipulated valuation methods

(c) Deadlock Abuse

- Artificial triggering of option clauses

(d) Regulatory Non-Compliance

- Especially in cross-border transactions

8. Drafting Best Practices (Governance Perspective)

- Clearly define trigger events

- Use independent valuation mechanisms

- Align with articles of association

- Include dispute resolution clauses (arbitration)

- Ensure compliance with securities law

Conclusion

Put–call options are powerful governance instruments that:

- Facilitate orderly exits

- Balance control and protection

- Reduce uncertainty in closely held companies

However, their effectiveness depends on:

- Careful drafting

- Alignment with fiduciary duties

- Judicial enforceability

Courts in the UK and similar jurisdictions generally uphold these mechanisms, but they intervene where unfair prejudice, improper purpose, or valuation manipulation is evident.

RELATED Blog

comments