Risk-Funding Alternative Structures.

1. Introduction to Risk-Funding Alternative Structures

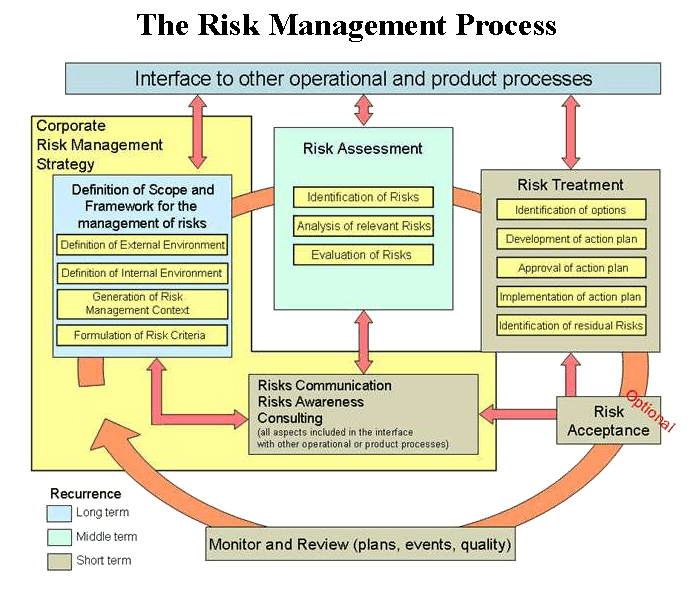

Risk-funding alternative structures refer to non-traditional methods of financing risk exposure, where organizations secure funds or mechanisms to absorb potential losses without relying solely on conventional insurance.

In essence, these structures determine how losses are financed when risks materialize.

2. Concept and Purpose

Traditional vs Alternative Risk Funding

| Traditional | Alternative |

|---|---|

| Insurance policies | Self-insurance / captives |

| Premium-based transfer | Capital market solutions |

| Risk transferred | Risk retained or shared |

Objectives

- Reduce insurance costs

- Improve cash flow efficiency

- Gain control over risk financing

- Access capital markets

3. Key Types of Alternative Risk-Funding Structures

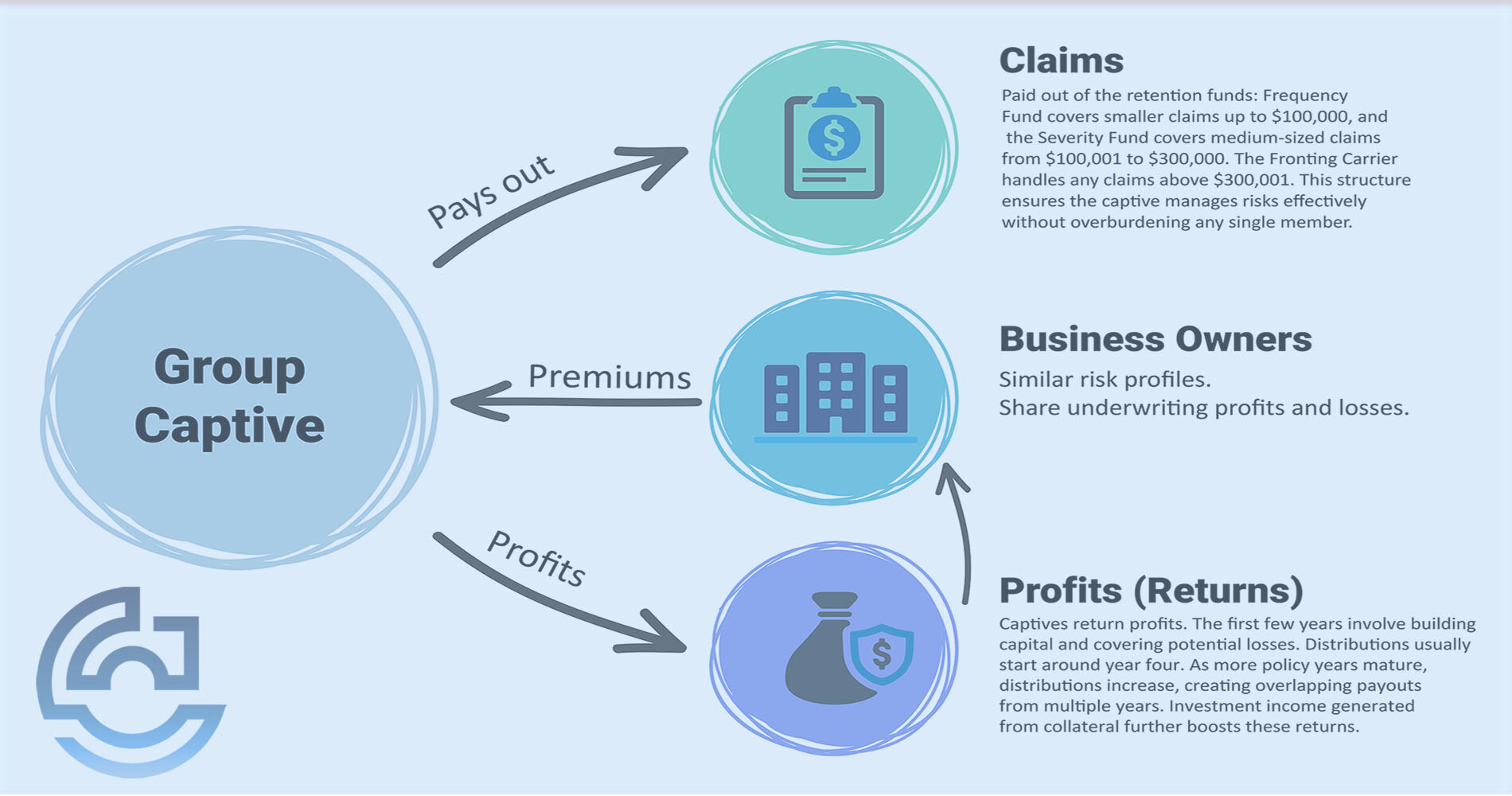

(A) Captive Insurance Companies

A captive insurer is a subsidiary created to insure risks of its parent company.

Features

- Parent retains risk internally

- Premiums paid to captive

- Profits retained within group

Types

- Single-parent captive

- Group captive

- Protected cell companies

(B) Self-Insurance

- Company sets aside reserves to cover losses

- No transfer to external insurer

Example

- Large corporations funding employee health claims internally

(C) Finite Risk Insurance

{kind=link}

- Combines risk transfer + financing

- Limited underwriting risk

- Focus on smoothing losses over time

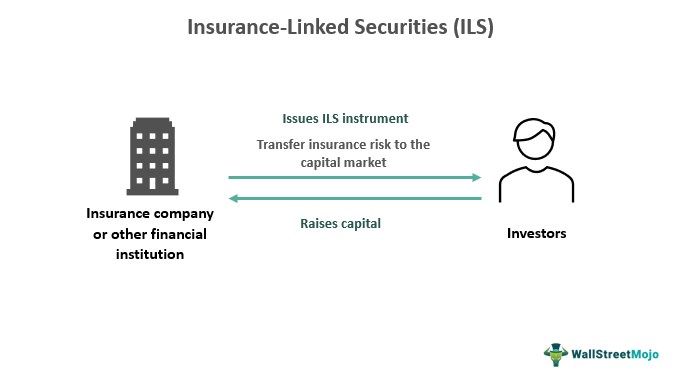

(D) Insurance-Linked Securities (ILS)

- Risks transferred to capital markets

- Investors bear risk in exchange for returns

Examples

- Catastrophe bonds (CAT bonds)

- Collateralized reinsurance

(E) Risk Retention Groups (RRGs)

- Group of companies pool risks

- Common in liability insurance sectors

(F) Contingent Capital Arrangements

- Pre-arranged funding triggered by events

- Includes:

- Standby credit facilities

- Loss-triggered equity issuance

4. Legal and Regulatory Framework

(A) Corporate Law

- Directors must ensure:

- Adequate funding of risks

- Proper disclosure

(B) Insurance Regulation

- Captives and ILS subject to:

- Licensing requirements

- Solvency rules

(C) Financial Regulation

- Capital adequacy norms

- Securitisation rules

(D) Tax Considerations

- Treatment of premiums, reserves, and offshore captives

5. Governance Considerations

(1) Board Oversight

- Approval of risk-funding strategy

(2) Risk Appetite Alignment

- Ensure funding matches risk tolerance

(3) Capital Adequacy

- Maintain sufficient reserves or funding capacity

(4) Transparency and Disclosure

- Investors must understand funding structures

(5) Regulatory Compliance

- Avoid misuse for tax evasion or risk concealment

6. Legal Issues and Risks

(1) Substance Over Form

- Courts examine whether structure genuinely transfers or funds risk

(2) Misrepresentation

- Failure to disclose true risk exposure

(3) Insolvency Risk

- Inadequate funding structures may collapse under stress

(4) Regulatory Arbitrage

- Use of structures to bypass regulatory requirements

7. Key Case Laws

1. HIH Casualty and General Insurance Ltd v Chase Manhattan Bank (2003)

- Principle: Risk funding structures cannot shield fraudulent conduct.

- Emphasized transparency in insurance-related arrangements.

2. Prudential Insurance Co Ltd v Inland Revenue Commissioners (1904)

- Principle: Defined nature of insurance vs non-insurance arrangements.

- Important in distinguishing alternative risk structures.

3. Re Lehman Brothers International (Europe) (2012)

- Principle: Structured financial arrangements for risk allocation/funding are enforceable if properly drafted.

4. Stone & Rolls Ltd v Moore Stephens (2009)

- Principle: Corporate structures used to manage risk may still attract liability if misused.

5. Caparo Industries plc v Dickman (1990)

- Principle: Duty of care in financial disclosure of risk exposures.

6. Lexington Insurance Co v Wasa International Insurance Co Ltd (2009)

- Principle: Interpretation of insurance structures depends on governing law and contractual wording.

7. Municipal Mutual Insurance Ltd v Sea Insurance Co Ltd (1998)

- Principle: Allocation and funding of insurance liabilities must follow contractual intent.

8. Practical Structuring Considerations

(1) Cost-Benefit Analysis

- Compare:

- Insurance premiums

- Cost of capital

(2) Risk Modeling

- Quantify potential losses

(3) Legal Structuring

- Ensure enforceability and compliance

(4) Diversification

- Combine multiple funding structures

(5) Documentation

- Clear contractual terms and disclosures

9. Advantages and Challenges

Advantages

- Cost efficiency

- Greater control over risk

- Access to capital markets

- Tailored solutions

Challenges

- Regulatory complexity

- High setup costs

- Risk of mispricing exposure

- Governance burden

10. Conclusion

Risk-funding alternative structures represent a strategic evolution beyond traditional insurance, enabling organizations to:

- Retain, transfer, or finance risks flexibly

- Optimize capital usage

- Enhance resilience

However, courts consistently emphasize that:

👉 These structures must be genuine, transparent, and properly governed

Otherwise, they risk:

- Legal invalidity

- Regulatory penalties

- Financial instability

RELATED Blog

comments